Having a short discussion with one of my friend met in one of the property investment seminar. He also bought into Pangsapuri Widuri at that time. I asked, ” How many have you invested after the Pangsapuri Widuri?”. His replied, “NONE”. My next question, “Why?” He is saying that his money has gone to his wedding. I follow up with another question, “Do you still believe property investment required a lot of money?”. His replied is “YES”.

Some of others investor also said that, at current market, it is hard to get positive cash flow. So not worth to invest in property. The rental market is so much depressed and the property price is high. Let do indepth mathematic calculations.

Say you bought into a residential property at RM500,000 in Penang near USM area.

Loan amount is RM500,000 x 90% = RM450,000

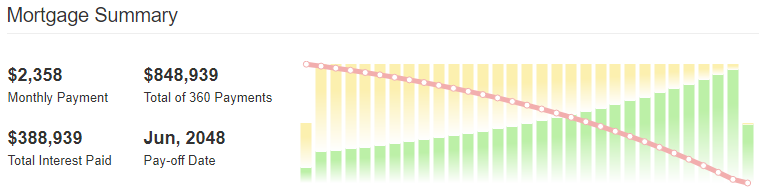

Monthly installment @ 4.6 % for 30 years = RM2,358

The rental is only able to fetch RM1,800 per month.

It simply means that RM1,800 – RM2,358 = -RM558 (negative Cash flow)

Source: https://www.amortization-calc.com/mortgage-calculator/

In normal circumstances, no investor will buy into this property as the negative cashflow is high. However, for Sophisticated Investor, he will invest into it. Do you know why?

Two component need to take into consideration, namely Capital Gain and Equity gain.

1st Consideration: Capital Gain

As we know, property price gain is through inflation. For Malaysia average inflation rate is 5% in average. As such, the property price will be valued at RM500,000 x 5% = RM25,000

2nd Consideration: Equity Gain

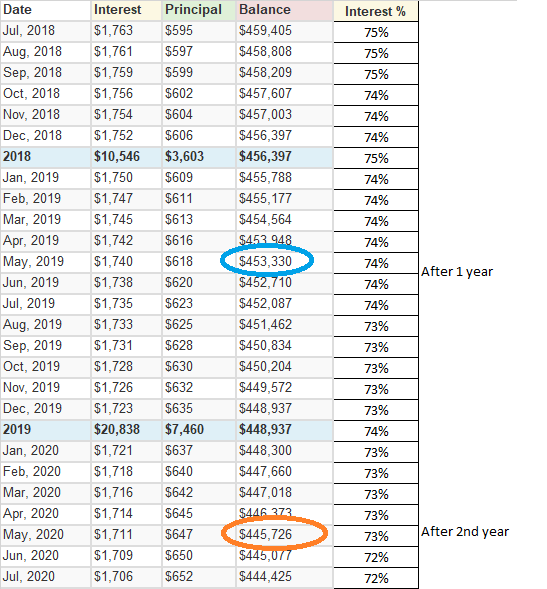

Let’s look at below details break down of the Loan Repayment schedule. It split to two portion, interest charged and Principal. The interest is about 75% of the total monthly installment for 1st year.

Your rental is RM1,800 and it match with your monthly interest charged. In a way, your tenant is paying for your bank interest charges. You as a landlord, you are paying your principal to the bank. You may treat this as a hard saving into the bank. If you can shift your thinking to this “SAVING” concept, then you are one step better than the normal investor. Let see, after 1 year. your loan balanced is reduced to RM453,330 (Blue circle). The starting loan is RM460,000, you have save RM6,670

With Capital Gain + Equity Gain = Total gain after 1 year

= RM25,000 + RM6,670

= RM31,670

What happen on 2nd year? Similarly, there is a Capital Gain and Equity gain on 2nd year.

Capital Gain = RM525,000 x 5% = RM26,250

Equity Gain = RM460,000 – RM445,726 (Red Circle)

= RM14,274

Total Gain on 2nd year = RM40,524

Your gain has growth from RM31,670 on first year to RM40,524 on second year.

And based on the Rule of 72, the property price will Double in 14.5 years.

Meaning, at year 15, your property value is at RM1 mil

The loan balanced at the year 15 is RM306,210 and your property is valued at RM1 mil. You just have the gain of approximately RM 693,790 in 15 years!

If you calculate your force saving amount = RM558 per month x 12 month x 15 years

= RM100,440

Your net gain = RM693,790 – RM100,440

= RM593,390 (out of no where!)

Would you buy into it? If you invested 2 units, after 15 years, you are RM1.2 mil richer compare to other if do not take actions and do above calculations! The prerequisite is you must be able to do force saving in negative cash flow property.