The property market is driven by several factors, including inflation. In this situation is basically an increase in the cost of goods and services broadly. Inflation affects property prices, particularly over the long term. Everyone is crying when the property price is escalating fast.

Let’s do some quick math for a property price when the annual inflation is 7%.

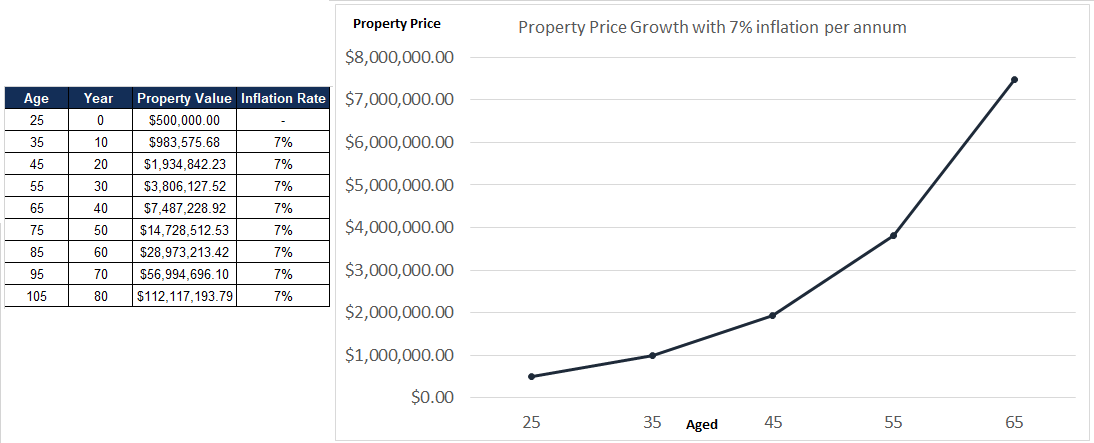

When a fresh graduate Mr Siva aged 25 years old, buy a property at RM500,000 for own stay. How would the property price escalate in the next 4o years?

According to the Rule of 72, with 7% inflation rate, the value of the property will double in every 10 years. Refer to the chart below, at the aged of 35 years old, the property price is at about RM983,575, say RM1,000,000. For the next 10 years, at the aged of 45 years old, the property price is at RM1,934,842, closed to RM2,000,000.

Mr Siva only do One important action at the age of 25 years old which is buy a property! For the remaining of the years, Mr Siva just serving his bank installment and yet the price of his house double in value in every 10 years.

You may imagined if Mr.Siva bought his 2nd house for investment, what will be his wealth grow?

At the aged of retirement (65 years old), Mr Siva has his retirement fund worth more than RM7,000,000 in equity. He can do whatever he want either sell off, rent a smaller unit, keep the cash, travel the world, buy a super car etc.

Conclusion

As a normal civilian in any part of the world, you can expect to pay more for all the goods you buy when inflation kicks in. Inflation is the reason why a roti canai costs about RM1.20 pr piece compared to RM0.50 10 years ago. Yet while inflation is an inevitable part of the economy, owning a piece of property can help you hedge against it peacefully.