This morning, my friend, Anthony shared with me Mr Wong portfolio and ask me if he can achieved similar portfolio when he is 50 years old.

First let see the summarize for Mr Wong portfolio as below

Mr Wong is a businessman and Mrs Wong is salaried employed. Both 50 years old. They have 3 children aged 15,17 & 22 years old.

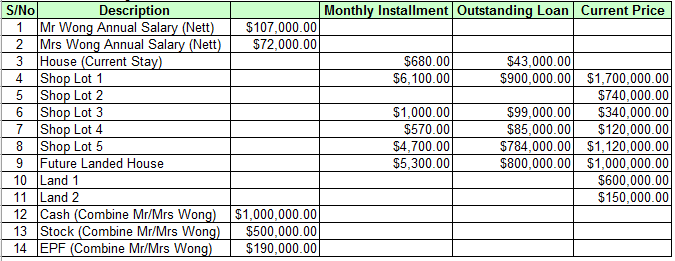

Table 1: Information given

Table 1 Information given

Based on the information given, the information is not really complete. The missing information such as if those shop houses is rented out with what rental? Another piece of information is missing is the household monthly expenses. I also cannot tell what is my friend want. Is he want to own 5 shop houses and 2 plot of lands? Or having the same cash as him?

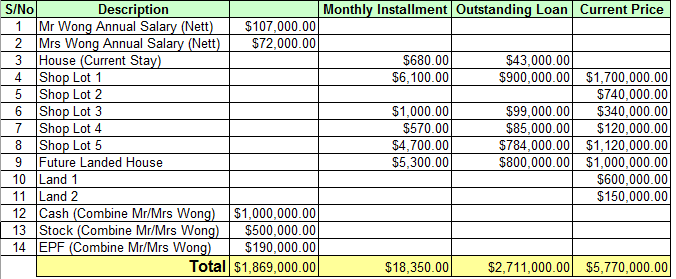

So I have to do the maths on those information given above. I have to do summation for all first with Table 2 below.

Table 2: Sum up all the numbers

Table 2 Sum up all the numbers

Their liquidity asset is $1.869 million.

Total liabilities is $2.711 million.

So Total Networth = Total Asset – Total Liabilities

= $1.69 m + $5.77 m – $2.711 m

= $4.749 m

As such with $4.75 million networth sound is good at the age of 50 years old. However, will they retired peacefully by the age 55 years old? This is a hard questions since there is no rental information on the shoplots, there will be better to assess the situation.

Assuming total 5 shop houses rent out and can get positive cash flow with $10K nett.

Will it be good? It is very good.

So I just demonstrate three index above,

- Liabilities

- Networth

- Cash flow

These are the main three factors for someone to consider during your wealth accumulations. Liabilities has to be reduced over time. Networth and cashflow has to increased over time.

Let’s get back to my friend first question, “Is possible for me to achieve Mr Wong portfolio?”

Now it will easier to answer after restructure the above information.

For your information my friend Anthony is only 30 years old.

My advice to him is to acquired asset that create positive cashflow. Networth will increased over time whilst liabilities will reduced accordingly.

For instance, say Anthony start to acquired one positive cash flow property per year.

This target is not aggressive at all and indeed very slow.

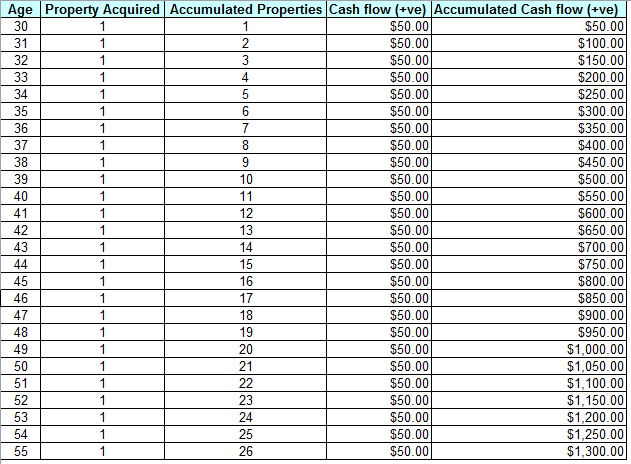

Strategy is as below:

- Buy 1 positive cash flow property every year from age 30 till 55 years old

- In below calculations, assume each property is having $50 per month

Let’s do the math:

Table 3 Acquisition

At the aged of 55 years old, Anthony had bought 26 properties and monthly net rental income is $1300 based on the conservative calculations.

26 years with inflation of 5% per annum, the asset also increased by 5% per year. Similiar to positive cash flow will increased. For the sake of calculations, what if the net rental for each property is $500, total net rental income will be $13k per month.

As such in order to achieve Mr Wong, cash flow, indeed it is possible and everyone can do it. Bear in mind this is slow and steady method.

Maybe by that time,Anthony can sell 6 properties and paid off the remaining 20 properties with no more monthly instalment. Whatever rental collected will be net rental income already. Can you imagine if the rental is $1000 per month, you will be having $20k income per month!

All depend on your strategy on what you want to achieve.

Source: http://www.forbes.com